Submissions for the Fall 2026 Capstone Project Are Open

Companies, nonprofits, and research labs! CDS invites proposals for a project for our Data Science MS students to work on during the Fall 2026 semester. Submit your proposal by August 2, 2026.

On this page: Overview • Fall 2025 Capstone Project List • Fall 2024 Capstone Project List • Best Fall 2024 & 2025 Capstone Posters

Overview

CDS master’s students have a unique opportunity to solve real-world problems through the capstone course in the final year of their program. The capstone course is designed to help students apply their knowledge to practical situations and develop critical skills such as problem-solving and collaboration.

Students are matched with research labs within the NYU community and industry partners to investigate pressing issues, applying data science to the following areas:

- Probability and statistical analyses

- Natural language processing

- Big Data analysis and modeling

- Machine learning and computational statistics

- Coding and software engineering

- Visualization modeling

- Neural networks

- Signal processing

- High-dimensional statistics

Capstone projects provide students with the opportunity to work in their field of interest and gain exposure to applicable solutions. Project sponsors, NYU labs, and external partners benefit from having a fresh perspective applied to their projects.

“Capstone is a unique opportunity for students to solve real-world problems through projects carried out in collaboration with industry partners or research labs within the NYU community,” says capstone advisor and former CDS Research Fellow Anastasios Noulas. “It is a vital experience for students ahead of their graduation and prior to entering the job market, as it helps them improve their skills, especially in problem-solving contexts that are atypical compared to standard courses offered in the curriculum. Cooperation within teams is another crucial skill built through the Capstone experience as projects are typically run across groups of 2 to 4 people.”

The Capstone Project offers organizations the chance to propose a project that our graduate students will work on as part of their curriculum for one semester. Information on the course, along with a questionnaire to propose a project, can be found on the Capstone Fall 2025 Project Submission Form.

Companies, nonprofits, and research labs! Interested in submitting a Capstone project proposal for students to work on? Please reach out to ds-capstone@nyu.edu.

The Capstone Project offers organizations the chance to propose a project that our graduate students will work on as part of their curriculum for one semester. Information on the course, along with a questionnaire to propose a project, can be found on the Capstone Fall 2026 Project Submission Form.

Fall 2025 Capstone Project List

- A Framework for Generative Music Models and Creator Tools with Ethical Licensing and Attribution

- Agentic AI for Automating People Discovery, Outreach, and Dashboard Generation at Scale

- Agentic AI Framework for Commercial Use Cases with MCP Compliance

- Agentic AI Operators for Freight Forwarder

- Agentic Health AI

- AI Agent for Exploratory Data Analysis and Anomaly Detection

- AI Assistant for Clinical Trial Protocol Design

- AI dectection tools for improving the quality of online research

- AI-Driven enhancement of Breast MRI interpretation using large-scale imaging and clinical data

- AI-Powered Pharmacovigilance System for Oncology Drug Safety Monitoring

- Assessing LLM Output Stability in Mental Health Applications

- AssetOpsBench: Benchmarking Autonomous Agents for Industrial Asset Operations

- Attention-Based Transformers for Transparent Survival Analysis

- Audio-Visual Speaker Diarization Leveraging Foundation Models

- Automating LLM-driven Counterfactual Data Generation

- Autonomous Agent for Real-Time Issuer related Event Detection and Impact Analysis

- Bibliometrics and LLMs for Transplant Knowledge Distillation

- Bridging DNA and Protein language models for multi-species regulatory sequence prediction

- Build a better resume screener

- Cognition-Aware Human Modeling for Semi-autonomous driving

- Context2SQL

- Delivering Elite Football (Soccer) Analytics

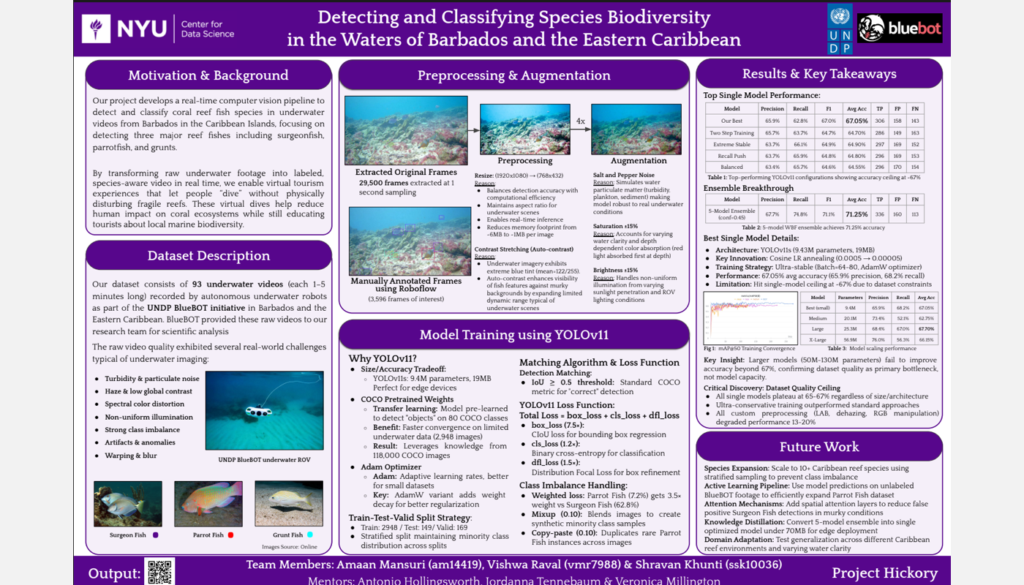

- Detecting and classifying species biodiversity in the waters of Barbados and the Eastern Caribbean

- Developing methods for large-scale data integration through semantic mappings

- Developing Multi-Modal Deep Learning Models for MRI Analysis

- Do LLMs produce gender bias in hiring?

- Exploring Perceptual Loss in Deep Learning-based MRI Image Reconstruction

- Generative Pre-Training (GPT) for Structured EHR data

- Improving Institutional Bitcoin Accumulation Strategies

- Improving Tokenization by optimizing BPE

- Machine Learning for Download Quality Detection

- Machine Learning for Entity Linking

- Model and predict videoconference communication experience quality using multimodal data

- Modeling Human Decision Conflict with the Substrate-Prism Neuron

- Multi-Agent Document Intelligence System

- Multimodal Foundation Models for Stroke Severity Prediction

- Overview | ACM ICAIF 2024 FinRL Contest

- Predicting Progression to Chronic Pancreatitis Using Time-to-Event AI on Longitudinal CT Data

- RAG framework and Agentic Health

- Recalled Experiences of Death (RED): A Natural Language Processing Approach to Determining its Themes and Distinguishing it from other Human Experiences.

- Shrinking human genes with generative modeling

- Specialized AI Platform for Clinic Decision-making Support in Cancer Therapeutics

- Strategic Funding Analytics: Predictive Modeling for EdTech Investment Opportunities

- Tiny Movements, Big Insights: Deep Learning for Infant Motion and Emotion Recognition from Video

- Transformer-based Causal Inference in the Real World

- Using AI to Create Synthetic Commercial Data Sets

Fall 2024 Capstone Project List

- A machine learning framework for identifying interacting DNA elements from multiomics data

- A Non-biased Resume Screener in the Public Interest

- Advanced AI Techniques for Dynamic Portfolio Management and Financial Forecasting

- AI Tools for Journalists

- AI-Driven Reimbursement Code Discovery for HealthTech Start-Ups

- AI-powered deconvolution of RNA-sequencing data data

- American Colleges and Universities As Social Networks

- Audio-Visual Speaker Diarization Leveraging Foundation Models

- Calculating Weights for Causal Inference using Wasserstein GANs

- Deep learning models for cryptocurrency price analysis

- Designed Validation Sets

- Detecting Cognitive Impairment in Patient-Provider Communication

- Developing Multimodal Detection Systems for Narratives Promoting Misleading Information

- Developing Real-Time World Insight Reports with Machine Learning and LLMs

- Digitizing P&ID into Industrial Knowledge Graphs

- Dual-RAG: Advanced Financial Video QA with Multimodal RAG system

- Enhanced Automatic Annotation of Spoken Adult-Child Interactions

- Enhancing Large Language Models for Psychiatric Assessment

- Estimation of a Latent Space Model for Strategic Network Formation

- Hepatocellular Carcinoma Recurrence Prediction Radiomics Model

- Improving genetic prediction of disease risk

- Improving MRI Image Reconstruction via Generative AI

- Information-constrained emergent communication

- Large Language Models Encode Search for Clinical Evidence in Cancer Therapeutics

- Learning to detect breast cancer utilizing all imaging modalities

- Life Time Value (LTV) Model

- Long-form Egocentric Video Understanding

- Machine Learning-Driven Performance Monitoring in NYU’s DWDM Optical Transport Network

- Model and predict videoconference communication experience quality using multimodal data

- Optimizing Generative AI Modeling Stack for Sophisticated Financial Question Answering

- Optimizing Kidney Composite Allocation Score Using Simulation Optimization

- Political Partisanship and the US Judicial System

- Power Grids and Markets: Quantitative Trading and Analysis

- Predicting Agency Project/Program Success

- Real-Time Interpretation and Translation for Low-Resource Languages

- Relational Deep Learning and Graph Neural Networks for Anti Money Laundering

- Scaling Satellite Imagery of Urban Streets via Automated Classification and OpenStreetMap

- Solar Foundation Models

- Spatial Morbidity and Co-morbidity in the U.S.

- Tofu’s Candidate Matching Model

- Understanding Distribution Shifts in Time

- Use AI and math tools to do real estate appraisals

- User-centric AI-models for assisting the visually impaired

- Utilize large language model to analyze radiology report

- Video representation learning

Best Fall 2024 and 2025 Capstone Posters

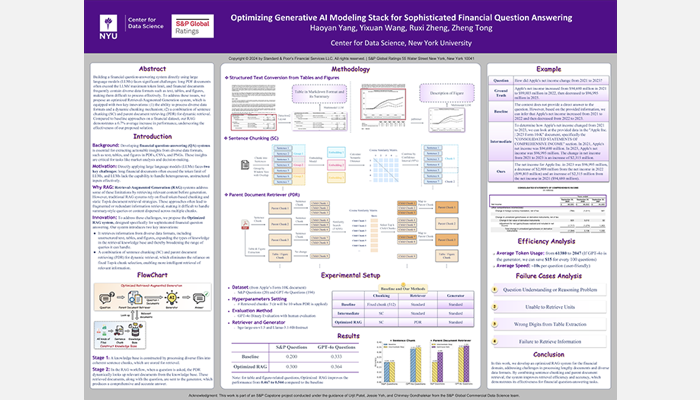

2024: Optimizing Generative AI Modeling Stack for Sophisticated Financial Question Answering

Student Authors: Haoyan Yang, Yixuan Wang, Ruxi Zheng, Zheng Tong

Project Mentors: Urjit Patel, Jessie Yeh, Chinmay Gondhalekar

© 2024 S&P Global Ratings

2025: Detecting and classifying species biodiversity in the waters of Barbados and the Eastern Caribbean

Student Authors: Amaan Mansuri, Vishwa Raval, Shravan Khunti

Project Mentor: United Nations Development Programme (UNDP)

2023 Posters

Best Fall 2023 Capstone Posters

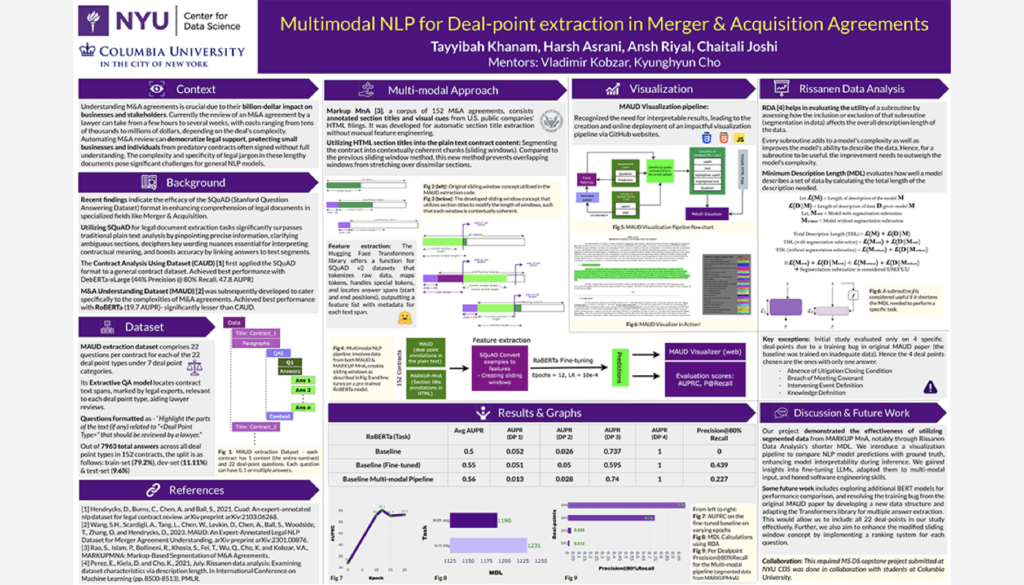

Multimodal NLP for M&A Agreements

Student Authors: Harsh Asrani, Chaitali Joshi, Tayyibah Khanam, Ansh Riyal | Project Mentors: Vlad Kobzar, Kyunghyun Cho

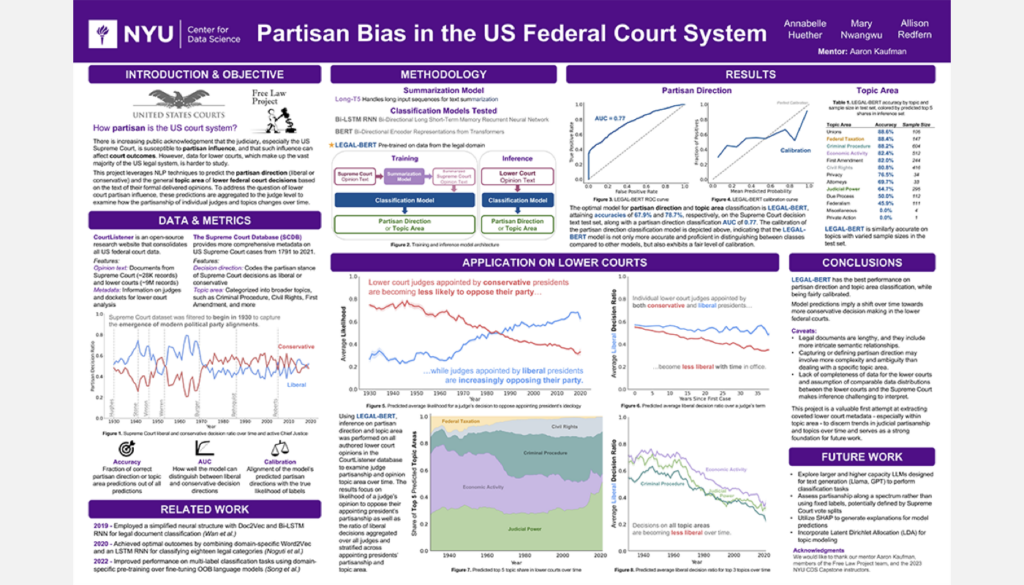

Partisan Bias and the US Federal Court System

Student Authors: Annabelle Huether, Mary Nwangwu, Allison Redfern | Project Mentors: Aaron Kaufman, Jon Rogowski

Best Fall 2023 Student Voted Posters

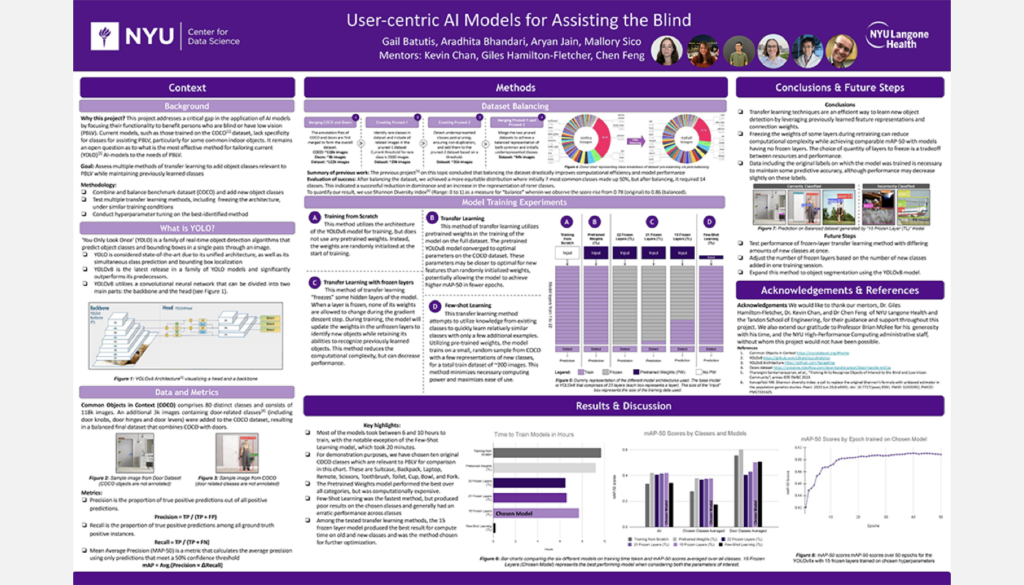

User-Centric AI Models for Assisting the Blind

Student Authors: Gail Batutis, Aradhita Bhandari, Aryan Jain, Mallory Sico | Project Mentors: Giles Hamilton-Fletcher, Chen Feng, Kevin C. Chan

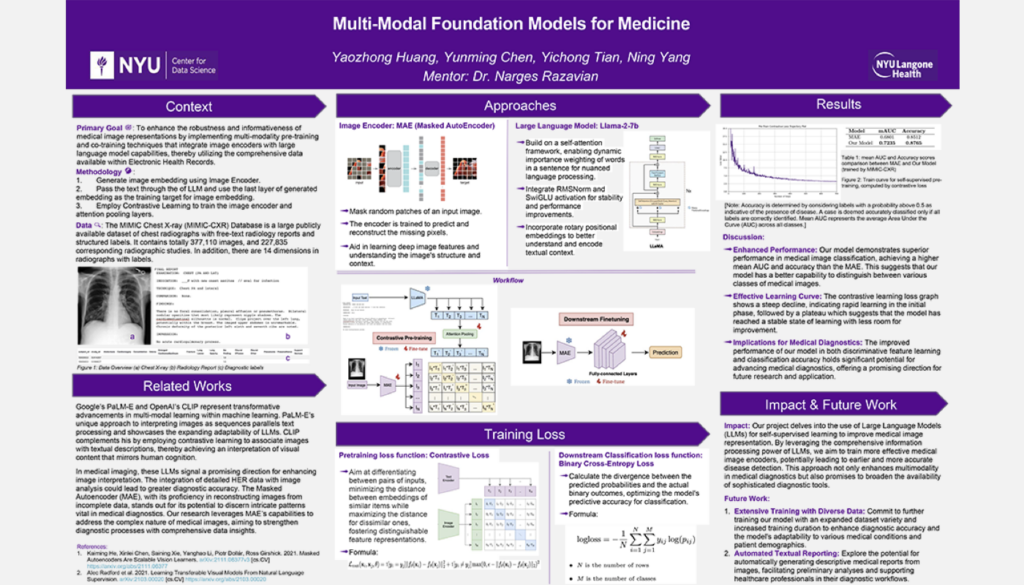

Multi-Modal Foundation Models for Medicine

Student Authors: Yunming Chen, Harry Huang, Jordan Tian, Ning Yang | Project Mentors: Narges Razavian

Best Fall 2023 Student Voted Runner-Up Posters

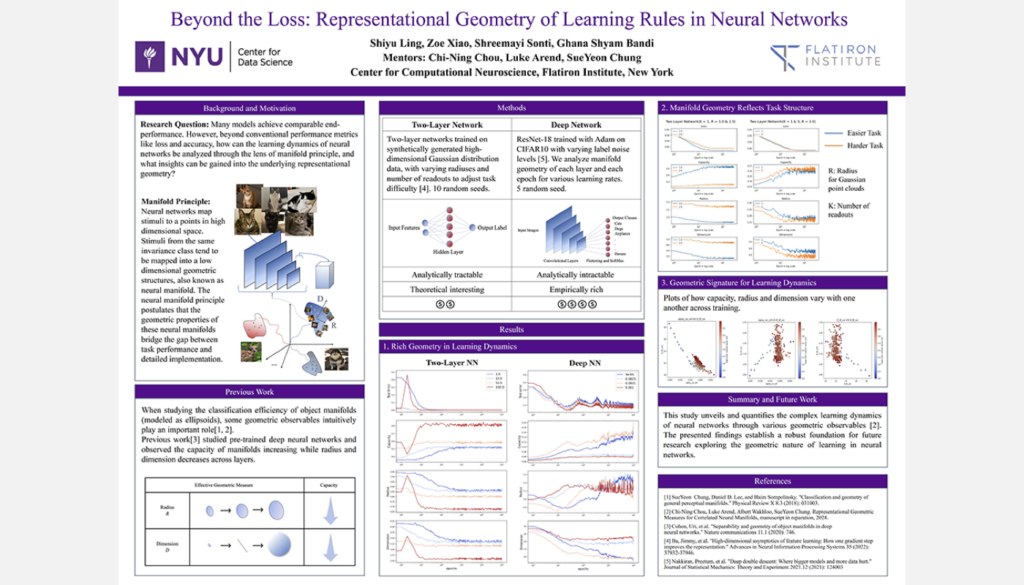

Representational Geometry of Learning Rules in Neural Networks

Student Authors: Ghana Bandi, Shiyu Ling, Shreemayi Sonti, Zoe Xiao | Project Mentors: SueYeon Chung, Chi-Ning Chou

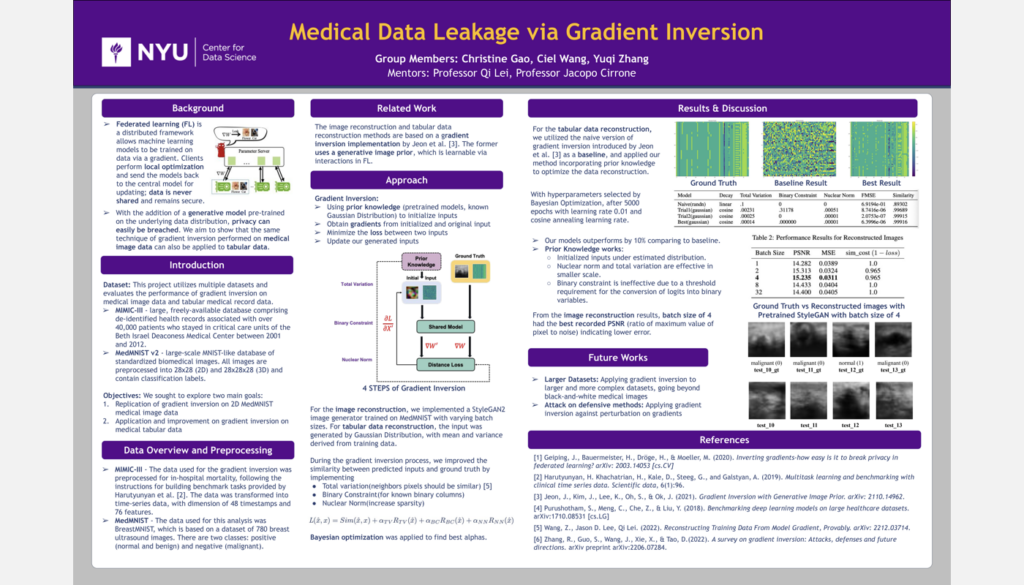

Medical Data Leakage with Multi-site Collaborative Training

Student Authors: Christine Gao, Ciel Wang, Yuqi Zhang | Project Mentors: Qi Lei

Fall 2023 Capstone Project List

- A machine learning model to predict future kidney function in patients undergoing treatment for kidney masses

- Advanced Name Screening and Entity Linking Using large language models

- Automated assessment of epilepsy subtypes using patient-generated language data

- Bringing Structure to Emergent Taxonomies from Open-Ended CMS Tags

- Build Models for Multilingual Medical Coding

- Building an Interactive Browser for Epigenomic & Functional Maps from the Viewpoint of Disease Association

- Causal GANs

- Designing Principled Training Methods for Deep Neural Networks

- Developing predictive shooting accuracy metric(s) for First-Person-Shooter esports

- Discovering misinformation narratives from suspended tweets using embedding-based clustering algorithms

- Does resolution matter for transfer learning with satellite imagery?

- Egocentric video zero-shot object detection

- Evaluating the Capability of Large Language Models to Measure Psychiatric Functioning

- Explanatory Modeling for Website Traffic Movements

- Extracting causal political narratives from text.

- Fine-Tuning of MedSAM for the Automated Segmentation of Musculoskeletal MRI for Bone Topology Evaluation and Radiomic Analysis

- Foundation Models for Brain Imaging

- Housing Price Forecasting – Alternative Approaches

- Identify & Summarize top key events for a given company from News Data using ML and NLP Models

- Improving Out-of-Distribution Generalization in Neural Models for Astrophics and Cosmology?

- Knowledge Extraction from Pathology Reports Using LLMs

- Leverage OncoKB’s Curated Literature Database to Build an NLP Biomarker Identifier

- Measuring Optimizer-Agnostic Hyperparameter Tuning Difficulty

- Medical Data Leakage with Multi-site Collaborative Training

- Metadata Extraction from Spoken Interactions Between Mothers and Young Children

- Multi-Modal Foundation Models for Medicine

- Multimodal NLP for M&A Agreements

- Multimodal Question Answering

- Network Intrusion Detection Systems using Machine Learning

- Online News Content Neural Network Recommendation Engine

- OptiComm: Maximizing Medical Communication Success with Advanced Analytics

- Partisan Bias and the US Federal Court System

- Predicting cancer drug response of patients from their alteration and clinical data

- Predicting year-end success using deep neural network (DNN) architecture

- Prediction of Acute Pancreatitis Severity Using CT Imaging and Deep Learning

- Preparing a Flood Risk Index for the State of Assam, India

- Representational geometry of learning rules in neural networks

- Segmentation of Metastatic Brain Tumors Using Deep Learning

- Social Network Analysis of Hospital Communication Networks

- Supporting Student Success through Pipeline Curricular Analysis

- Transformers for Electronic Health Records

- Uncertainty Radius Selection in Distributionally Robust Portfolio Optimization

- Unveiling Insights into Employee Benefit Plans and Insurance Dynamics

- User-centric AI models for assisting the blind

- Using Deep Learning to Solve Forward-Backward Stochastic Differential Equations

- What Keeps the Public Safe While Avoiding Excessive Use of Incarceration? Supporting Data-Centered Decision-making in a DA’s Office